Fixed index annuities offer a conservative way to benefit from gains in the market without putting your principal at risk. Additional benefits include tax-deferred growth and guaranteed minimum returns. But there are also caps on growth you can experience, and contracts can be complex.

Christian Simmons, CEPF Financial Writer, Certified Educator in Personal Finance Christian Simmons is a financial writer who has worked professionally as a journalist since 2016. As an active member of the Association for Financial Counseling & Planning (AFCPE), Christian prides himself on his ability to break down complex financial topics in ways that Annuity.org readers can easily understand. Read More

Lamia Chowdhury Financial Editor Lamia Chowdhury is a financial editor at Annuity.org. Lamia carries an extensive skillset in the content marketing field, and her work as a copywriter spans industries as diverse as finance, health care, travel and restaurants. Read More

Rubina K. Hossain, CFP® Client Advisor for MEIRA Certified Financial Planner Rubina K. Hossain is chair of the CFP Board's Council of Examinations and past president of the Financial Planning Association. She specializes in preparing and presenting sound holistic financial plans to ensure her clients achieve their goals. Read More

Fact Checked Fact CheckedAnnuity.org partners with outside experts to ensure we are providing accurate financial content.

These reviewers are industry leaders and professional writers who regularly contribute to reputable publications such as the Wall Street Journal and The New York Times.

Our expert reviewers review our articles and recommend changes to ensure we are upholding our high standards for accuracy and professionalism.

Our expert reviewers hold advanced degrees and certifications and have years of experience with personal finances, retirement planning and investments.

How to Cite Annuity.org's ArticleAPA Annuity.org (2024, September 11). Fixed Index Annuity Pros and Cons. Retrieved September 14, 2024, from https://www.annuity.org/annuities/types/indexed/pros-and-cons/

MLA "Fixed Index Annuity Pros and Cons." Annuity.org, 11 Sep 2024, https://www.annuity.org/annuities/types/indexed/pros-and-cons/.

Chicago Annuity.org. "Fixed Index Annuity Pros and Cons." Last modified September 11, 2024. https://www.annuity.org/annuities/types/indexed/pros-and-cons/.

Why Trust Annuity.org Why You Can Trust Annuity.orgAnnuity.org has provided reliable, accurate financial information to consumers since 2013. We adhere to ethical journalism practices, including presenting honest, unbiased information that follows Associated Press style guidelines and reporting facts from reliable, attributed sources. Our objective is to deliver the most comprehensive explanation of annuities and financial literacy topics using plain, straightforward language.

We pride ourselves on partnering with professionals like those from Senior Market Sales (SMS) — a market leader with over 30 years of experience in the insurance industry — who offer personalized retirement solutions for consumers across the country. Our relationships with partners including SMS and Insuractive, the company’s consumer-facing branch, allow us to facilitate the sale of annuities and other retirement-oriented financial products to consumers who are looking to purchase safe and reliable solutions to fill gaps in their retirement income. We are compensated when we produce legitimate inquiries, and that compensation helps make Annuity.org an even stronger resource for our audience. We may also, at times, sell lead data to partners in our network in order to best connect consumers to the information they request. Readers are in no way obligated to use our partners’ services to access the free resources on Annuity.org.

Annuity.org carefully selects partners who share a common goal of educating consumers and helping them select the most appropriate product for their unique financial and lifestyle goals. Our network of advisors will never recommend products that are not right for the consumer, nor will Annuity.org. Additionally, Annuity.org operates independently of its partners and has complete editorial control over the information we publish.

Our vision is to provide users with the highest quality information possible about their financial options and empower them to make informed decisions based on their unique needs.

A fixed index annuity is a long-term savings product whose return is based on a stock market index. While fixed index annuities are often tied to major market indexes such as the S&P 500, they can also be tied to less common indexes depending on the financial institution or insurer that sells them.

Unlike stocks and other types of annuities, fixed index annuities provide security against losses if the market falls. A contract typically ensures that you will never lose your principal in exchange for a cap on potential earnings. Similar to other annuities, they are intended to provide a steady income stream during retirement and can be used to round out a 60/40 investment portfolio.

But along with a cap on earnings, fixed index annuities are generally illiquid, and contracts can be complex.

It’s essential to weigh the pros and cons of a fixed index annuity before determining if one is right for you.

Is An Annuity Right For You?

Our short quiz provides clarity on whether an annuity is a smart choice for your retirement portfolio.

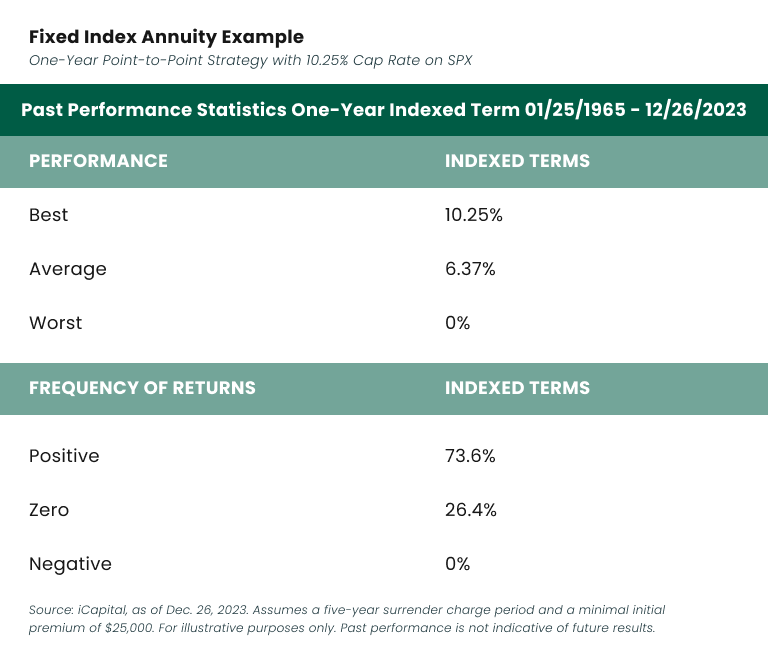

Fixed index annuities are generally safe products because they are designed to protect investors from market downturns while still allowing them to benefit from upswings.

Buying a fixed index annuity is typically structured in a format where you see limited losses when the index it’s tied to declines but benefit from a percentage of the growth when that index improves.

Different products offer several crediting strategies, with options ranging from different indexes to selecting floors and caps that make sense for you.

A floor places a percentage limit on how much you can lose — and a minimum on how much you can earn. For example, if the floor is set at 5% and the index decreases by 12%, you would only lose 5% of your contract value.

Another potential benefit of a fixed index annuity is that the company issuing the product may include a minimum return guarantee.

This means that — even if the index your annuity is tied to declines — you can still experience a small, guaranteed amount of growth. This adds an extra level of safety to the product, guaranteeing you at least some level of return.

In some ways, fixed index annuities operate similarly to CDs by presenting a safe way to grow your money at a solid rate. The main difference, of course, is that fixed index annuities base their rate of growth on an index while CDs generally offer a fixed rate.

That chance to participate in the market’s upside allows fixed index annuities to offer potentially higher returns than CDs.

Additionally, the tax deferral component offered through fixed index annuities is not available with a CD. This means your money can grow even more than it would in a CD since your interest can go untaxed while it grows.

Indexed Annuities have a 3.27% average annual return*

*Based on a study from 2007-2012

CDs have a 1.76% average annual return*

*Based on 12-month CDs from 12/31/2001-12/31/2020

Tax-deferral is a significant benefit of opting for a fixed index annuity since it’s a feature not commonly available through many financial products.

When you purchase an annuity, you will only owe taxes once you withdraw money from the product. This is a notable difference from a CD, where you pay tax on the annual interest earned.

Since the money in your annuity account is untaxed, you have the opportunity for even more growth since that money can continue to compound on itself uninhibited through the course of your contract term.